Traditional European banks often fall short when it comes to flexibility and returns on uninvested cash.

That’s why more people are turning to digital solutions that offer higher interest on idle cash, fewer bureaucratic hurdles, and cheaper currency conversion abroad.

In this article, we’ll explore some of the top online banking options in Europe, highlighting the pros and cons of each so you can choose the one that best fits your needs.

Best Online Banks

- Revolut: The best digital bank in Europe overall. Best if you want to spend and withdraw in several different currencies, invest, and earn interest.

- Wise: Best for ultra-cheap international transfers in different currencies. On the downside, it does not hold a banking license.

- N26: Best if you want to have a free EUR IBAN bank account. It’s the smart, mobile-first bank designed for seamless banking anytime, anywhere. New users earn a bonus with our referral code.

- OpenBank: Best if you value safety and track record - it is part of Santander group. A fully digital bank offering simple, transparent, and innovative banking solutions.

- Trade Republic: Best for earning interest on your cash and getting cashback on spendings. It’s an investment platform that offers low-cost trading and automated savings.

- Monese: A solid alternative to Revolut or N26, good to diversity. A solid choice for expats and frequent travellers looking for a multi-currency account that works across borders. On the downside, it does not offer a banking license.

- Bunq: Another great European digital bank. Perfect for multi-currency accounts, instant payments and powerful budgeting tools.

- Tomorrow: Best if you value sustainability. It’s a digital bank for anyone who wants sustainable, transparent banking - with solid features and a clear positive impact. On the downside, accounts open only for DE/AT/IT/ES residents.

Comparison

When choosing an online bank, it all comes down to what matters most to you. In the comparison below, we break down four key features people typically look for:

- Money Protection – The level of protection your money has (e.g., whether it is covered by a deposit guarantee scheme).

- Multi-currency Accounts – Whether you can hold and manage money in different currencies.

- Free International Transfers – The ability to send money abroad without paying extra fees.

- Interest on Available Balance (Nominal Rate) – The rate you earn on money that’s sitting in your account, not yet invested.

These criteria will help you find the account that best aligns with your financial goals and lifestyle.

Interest on available balance shown as nominal rate, as of June 2026.

What is an Online Bank?

Before diving into the pros and cons of each option, it’s important to clarify what we mean by a digital bank.

A digital bank is a financial institution that operates primarily online, often without any physical branches. Everything - from opening an account to managing your money - is done through the internet or a mobile app. This also means that account setup can usually be done entirely remotely, without needing to visit a branch in person.

Because digital banks don’t carry the costs of maintaining physical locations, they can pass those savings on to customers - often offering lower fees and more flexible services. Many of them also provide extended customer support hours, sometimes even 24/7.

When it comes to safety, as long as the digital bank is licensed and regulated by official financial authorities (such as the central bank of the country where it operates), your money is protected - typically under the country’s deposit guarantee scheme, just like with traditional banks.

In-depth analysis of each online bank

Revolut

Revolut is an international fintech company that operates as an online bank, offering a fully online experience through its mobile app. Founded in the UK, it is now available across multiple European countries (check the full list of supported countries) and allows users to open an account quickly using only their phone.

One of its main advantages is how easy and affordable it is to make international payments. Currency conversion is done at highly competitive interbank rates, and the app supports accounts in multiple currencies with automatic exchange features. This makes it an excellent choice for frequent travellers and online shoppers who buy from international websites in different currencies.

Revolut also offers interest on uninvested balances, especially for users on paid plans, which can be higher than traditional banks in some cases. This option is available only for some countries.

The free Standard plan includes basic banking services with no monthly fee. There are also premium plans available that provide extra perks such as travel insurance, higher currency exchange limits, airport lounge access, and more.

Like most digital banks, Revolut supports instant transfers and complete account management via the app. However, it does not support cash deposits.

Finally, it’s important to note that Revolut holds a European banking license, meaning that deposits up to €100,000 are protected by the Lithuanian Deposit Guarantee Scheme - adding an extra layer of security for European users.

Pros:

- Multi-currency account with real exchange rates

- Attractive interest rates on uninvested cash

- No monthly fees on the standard account

Cons:

- Cash deposits not supported

- Free plan has usage limits, especially for currency exchange and ATM withdrawals

Wise

Wise (formerly TransferWise) is not technically a bank, but a licensed electronic money institution, regulated by the Financial Conduct Authority in the UK and the National Bank of Belgium in Europe.

Despite not being a traditional bank, it has become one of the most trusted and efficient platforms for people who work remotely, travel frequently or live between countries.

One of Wise’s biggest advantages is the multi-currency account, which allows users to hold, send, and receive money in over 50 currencies. You also get local bank details (IBAN/account numbers) for multiple regions - including the Eurozone, UK, USA, Australia and more - making it feel like you have bank accounts in several countries at once.

The platform is known for its low-cost and transparent currency exchange, using real exchange rates (mid-market rate) and clearly showing the fees upfront - no hidden surprises. This makes it ideal for transferring money abroad or spending in foreign currencies.

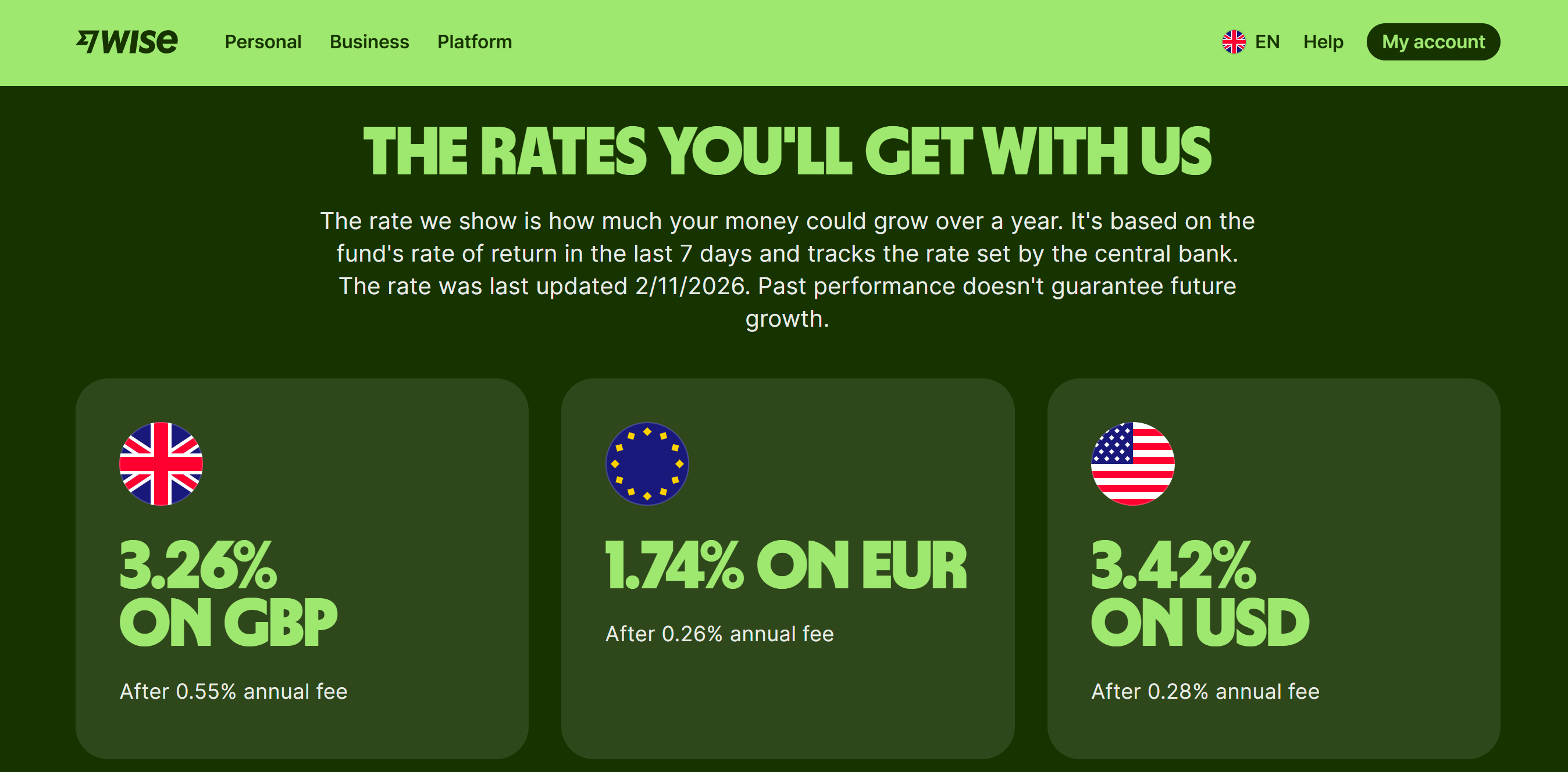

Although Wise doesn’t offer credit or investment products like traditional banks, it does allow users to earn interest on balances in some currencies, such as EUR, USD and GBP, by opting in to its interest-earning feature.

Pros:

- Low fees for international transfers

- Multi-currency account with local bank details

- Interest on available funds

Cons:

- Not a full bank (no loans, credit cards or other financial products)

- Cash deposits not supported

- Deposits are not protected by the Deposit Guarantee Fund

N26

N26 is a German digital bank that offers a fully mobile banking experience across Europe, focusing on simplicity and transparency. Users can open an account quickly via the smartphone app without needing to visit a branch.

One of N26’s main advantages is its intuitive app interface, which provides real-time notifications for transactions and easy money management. The basic account has no monthly fees and offers free ATM withdrawals within the Eurozone up to certain limits.

N26 supports multiple currencies and international payments, making it convenient for travellers and expatriates. The bank also provides premium accounts with added benefits like travel insurance, higher withdrawal limits, and dedicated customer support.

Like many online banks, N26 does not have physical branches, which may be inconvenient for customers who prefer face-to-face service. Customer support is primarily digital, via app chat or email.

N26 holds a European banking license, ensuring that deposits up to €100,000 are protected by the German Deposit Guarantee Scheme, providing strong security for users.

Pros:

- No monthly fees on the basic account

- Free ATM withdrawals in the Eurozone (up to a limit)

- Multi-currency accounts and cards available

- Deposits are protected by the Deposit Guarantee Fund

Cons:

- Limited product range compared to traditional banks

- Some features only available in premium plans

OpenBank

Openbank is a Spanish fully digital bank and a subsidiary of Banco Santander, offering a comprehensive range of banking products through its online platform.

Openbank allows customers to open accounts online without paperwork and offers a transparent fee structure. It is currently available in Spain, Portugal, Germany, and the Netherlands.

It offers various products, including current accounts, savings accounts, loans, and investment options, all accessible via its website or mobile app.

One key advantage of Openbank is its strong integration with investment services, appealing to users interested in managing their money and growing their wealth digitally. It also offers competitive fees and no account maintenance charges for basic accounts.

Customer service is mainly online, with phone and chat support.

As part of Banco Santander, Openbank benefits from robust financial backing and protection, with deposits covered up to €100,000 by the Spanish Deposit Guarantee Fund.

Pros:

- No account maintenance charge for basic accounts

- Wide range of banking products (accounts, loans, investments)

- Good integration with investment options

- Deposits are protected by the Spanish Deposit Guarantee Fund

Cons:

- Limited international services compared to some fintechs

- Slower account opening process for non Spanish

- Limited compatibility with digital wallets in some countries (Services like Apple Pay or Google Pay may not be supported)

Trade Republic

Although Trade Republic is primarily an investment platform, we chose to include it in this list because it also offers a debit card and pays interest on uninvested cash. This makes it a potentially useful option for those looking to combine saving and investing in one place. The platform is regulated in Germany and is available in several European countries.

Opening an account is fully digital and takes just a few minutes through the app or website. Users can invest in a wide range of assets, including stocks, ETFs, cryptocurrencies, and savings plans - all with low fees and a simplified interface.

One of Trade Republic’s key advantages is its flat fee model: most trades cost just €1 per order, with no custody or account maintenance fees. This transparent pricing appeals particularly to beginner investors and those who want to invest regularly without high costs.

The platform also offers ETF savings plans, allowing users to automate their investments from as little as €1 per month, which is ideal for long-term, passive investing strategies.

On these automatic investments there is no trade cost, which is a good advantage.

In addition to investing, Trade Republic now offers a debit card that can be used for everyday purchases.

What sets it apart is the "saveback" feature: every time you use the card, 1% of the amount spent is automatically set aside and invested into your selected savings plan, essentially turning your spending into a form of passive investing.

All deposits are held in a German partner bank and are protected up to €100,000 under the German Deposit Guarantee Scheme. Learn more about Trade Republic’s safety here.

Pros:

- No account or card maintenance charge

- Interest on uninvested cash (paid every month)

- Saveback feature (1% of your spends)

- Deposits are protected by the German Deposit Guarantee Fund

Cons:

- Not designed for everyday banking

- Lacks financial services such as: money transfers and currency exchange

- Customer support can be slow

Monese

Monese is designed for people on the move (expats, freelancers, or anyone without a permanent address) as it lets you open a UK or European IBAN account in minutes, without proof of address or credit checks. It’s a solid choice for those who want quick setup and don’t need advanced features.

You can hold money in GBP, EUR, and RON, and make international transfers through a partnership with Wise - though these are not always free unless you’re on a paid plan. Multi-currency support makes it convenient for frequent travellers or people living between countries.

Monese doesn’t currently offer savings accounts, investments, or credit products like loans or overdrafts. Some extra features include budgeting tools, virtual cards, and integration with Apple Pay and Google Pay.

Monese is not a bank but an e-money institution, so your funds are safeguarded under EU and UK regulations (rather than protected by deposit guarantee schemes). In practice, this means your money is held separately from Monese’s operational funds and cannot be used for lending. However, your money is not protected under any money protection scheme.

Pros:

- No account or card maintenance charge (on standard plan)

- Supports GBP, EUR, and RON accounts

- Virtual cards and Apple/Google Pay integration

Cons:

- No investments, credits or interest available

- Deposits are not protected by deposit guarantee schemes like in other online banks

Bunq

Bunq is a Dutch digital bank known for its user-friendly interface and a strong focus on sustainability and customization. It offers multi-currency accounts, free SEPA payments, and innovative features like multiple sub-accounts ("pots"), instant payments, and real-time spending insights.

Bunq is ideal for users who want control and flexibility, especially frequent travellers and freelancers.

While Bunq offers some interest on certain balances, its fees tend to be higher than competitors, and advanced features often require paid subscriptions (including cashback, loyalty cards and autosave). Additionally, it doesn’t provide traditional credit products like loans.

Bunq is fully regulated by Dutch authorities, with deposits protected under the Dutch deposit guarantee scheme up to €100,000.

Pros:

- Multi-currency accounts and multiple sub-accounts ("pots")

- Deposit protection up to €100,000 under Dutch scheme

Cons:

- Higher fees compared to some competitors

- Most advanced features require paid plans

Tomorrow

Tomorrow is a German-based digital bank that blends modern banking features with a strong environmental mission. Every euro you spend contributes to sustainable projects, from reforestation to clean energy - making it a favourite among users who want their money to reflect their values.

Currently, Tomorrow accounts are available only to residents of Germany, Austria, Italy, and Spain. You must have an official address in one of these countries to be eligible to open an account.

The app offers a clean, intuitive interface with features like sub-accounts ("pockets"), real-time tracking, and carbon footprint insights. Tomorrow supports free SEPA transfers, virtual cards, connection to Apple/Google Pay, and some plans even include cashback and travel insurance.

You can earn interest on savings in specific plans (via climate-friendly investment funds), but Tomorrow is not a multi-currency account - it only works in euros. Also, while it offers a few extras, it doesn’t yet include credit products like loans or overdrafts.

Deposits are protected under the German deposit guarantee scheme (up to €100,000), as Tomorrow operates through Solarisbank, a fully licensed financial institution.

Pros:

- Eco-conscious banking with certified climate impact

- Optional interest via sustainable investments

- Deposit protection up to €100,000

Cons:

- No multi-currency accounts

- Most advanced features require paid plans

- Limited to eurozone users

Which Bank to Choose?

Choosing the best fully digital bank depends on what matters most to you - security, features, or flexibility. Take a good look at the pros and cons of each option and think about how they match your needs and lifestyle.

Need a bank that makes international payments easy and supports multiple currencies? Revolut, Wise, and Bunq offer excellent flexibility for travellers and expats.

Looking for interest on your balance or simple ways to grow your money? Check out Trade Republic, Revolut, Openbank, or Tomorrow.

Prefer an easy, straightforward app for day-to-day spending and budgeting? Monese, N26, Revolut, or Bunq could be the perfect fit.

The good news? Most of these options have no maintenance fees, so you can try one -or even two - without risk and see which one feels right for you.

.png)