The best accumulating ETFs in 2026 (& how to invest)

You’ve probably heard about the wonders of compound interest and already have an idea of the impact that interest on interest can have in the long term, even though you might barely feel this effect at the beginning of your investment journey.

In this article, we’ll explain what accumulating ETFs are, their importance for long-term investing, the difference compared to distributing ETFs, their tax implications, and more!

What is an ETF?

For those reading this article, this might seem like a basic question, but many investors confuse the investment vehicle (the ETF) with what’s inside it. Let’s break it down:

An ETF (Exchange-Traded Fund) is a financial product that is traded on the stock exchange like a stock and aims to replicate the performance of a benchmark index.

For example, an ETF tracking the S&P 500 will be composed of stocks from companies in that index (what we call the “underlying assets”). However, an ETF can contain other asset classes besides stocks, such as bonds, real estate, commodities, and alternative investments. What I mean by this is that an ETF is not synonymous with stock investing, as is often mistakenly mentioned by some investors.

Since there can be many underlying assets within a single product (a mix of asset classes or a focus on a single asset class), ETFs allow you to easily diversify your portfolio at a low cost.

What is an Accumulating ETF?

An accumulating ETF is a type of ETF that automatically reinvests dividends, interest, or other income received from the underlying assets. You don’t receive these payouts in your brokerage account; instead, they are accumulated within the ETF itself, increasing its value.

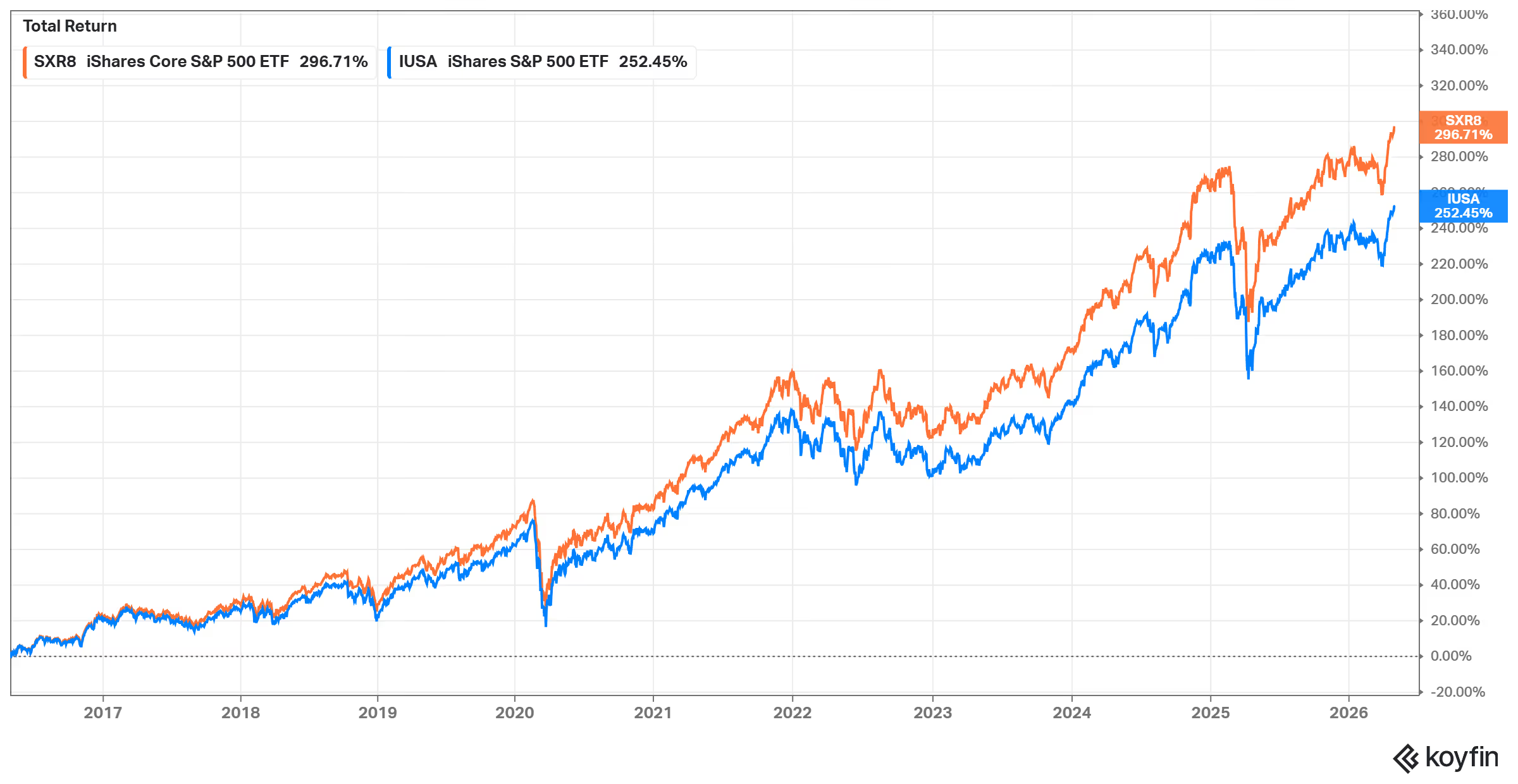

To better understand this dynamic, let’s look at a graphical representation. Below, we compare two versions of the same ETF: the iShares Core S&P 500 UCITS ETF USD, which, as the name suggests, replicates the performance of the U.S. stock index S&P 500. Here are the two versions:

- SXR8: Represents the accumulating version.

- IUSA: Represents the distributing version.

As you can see, the SXR8 gradually pulls away from the IUSA due to the effect of accumulation. If we looked at the total return (instead of price return), which includes dividends, interest, or other income received, the graphs would align (assuming full reinvestment of income, ignoring taxes or other costs).

However, in Portugal and several other European countries, investing in distributing ETFs is tax-inefficient. Let’s imagine a €10 dividend distribution. This amount would be subject to a 28% tax rate, meaning your net income would be €7.20. This is the amount you could reinvest. In contrast, with an accumulating ETF, the same €10 is not taxed.

Unlike distributing ETFs, which pay income directly to you (immediately subject to tax), accumulating ETFs use that income to buy more shares within the ETF, deferring taxation until the moment of sale (if there are realized gains).

How to choose the best accumulating ETFs?

Given the points mentioned earlier regarding asset classes, we can’t say that, for example, a stock ETF is better or worse than a bond ETF. Each has its own characteristics, such as risk level and underlying assets.

That said, there are attributes common to all ETFs that should be considered:

- Annual Cost: The annual cost of managing the ETF, also known as the Total Expense Ratio (TER), is one of the most important factors when choosing any ETF. Typically, opt for ETFs with a TER below 0.20%. Above this, it may be considered “expensive.” For example, if you invest €10,000, a 0.20% fee means you pay only €20 per year.

- Assets Under Management (AUM): The total value invested by all investors in an ETF is called “assets under management.” Generally, you should avoid ETFs with less than €100 million in AUM, as this increases the risk of the ETF closing because it’s not profitable for the management company to keep it active. However, if you’re invested in an ETF that decides to close, the assets within it are sold, and the resulting capital is distributed to investors—meaning you don’t lose your money.

- Age and Performance of the ETF: The longer an ETF has existed, the greater the confidence in its ability to fulfill its investment policy: replicating the performance of a specific index. Ideally, the relationship between an index and an ETF would be “1 to 1,” but factors like transaction costs, management team salaries, taxes, regulatory fees, and others prevent perfect replication. The difference between an ETF’s actual return and the index’s return is called the “tracking difference.” The smaller this difference, the better.

- Replication Method: How does the ETF achieve performance similar to the index it aims to replicate? There are two ways to gain this exposure:

- Physical: The ETF holds the same securities as the index, in the same proportions, to provide performance as close as possible to the index. There’s also a “simplified” version, where instead of buying all the index’s assets, it buys a representative sample (reducing costs).

- Synthetic: The index’s performance is replicated through swaps (financial derivatives). Swaps are typically provided by institutions like investment banks with the “promise” of delivering the same return as the index. Here, there’s counterparty risk, which, in our opinion, adds an unrewarded risk.

What are the best accumulating ETFs?

As mentioned earlier, there’s no “best,” but we can provide some examples across different asset classes:

Stocks:

- SPDR MSCI World UCITS ETF (Global stock ETF) => ISIN: IE00BFY0GT14

- iShares Core MSCI World UCITS ETF USD (Acc) (Global stock ETF) => ISIN: IE00B4L5Y983

- iShares Core S&P 500 UCITS ETF USD (Acc) (S&P 500 ETF) => ISIN: IE00B5BMR087

Bonds:

- iShares Core Global Aggregate Bond UCITS ETF EUR Hedged (Global bond ETF) => ISIN: IE00BDBRDM35

- iShares Core EUR Corporate Bond UCITS ETF (Acc) (Euro corporate bond ETF) => ISIN: IE00BF11F565

- Xtrackers II Eurozone Government Bond UCITS ETF 1C (Eurozone government bond ETF) => ISIN: LU0290355717

Mixed Funds (Stocks + Bonds):

- Vanguard LifeStrategy 20% Equity UCITS ETF (EUR) Accumulating (20% stocks, 80% bonds) => ISIN: IE00BMVB5K07

- Vanguard LifeStrategy 40% Equity UCITS ETF (EUR) Accumulating (40% stocks, 60% bonds) => ISIN: IE00BMVB5M21

- Vanguard LifeStrategy 60% Equity UCITS ETF (EUR) Accumulating (60% stocks, 40% bonds) => ISIN: IE00BMVB5P51

- Vanguard LifeStrategy 80% Equity UCITS ETF (EUR) Accumulating (80% stocks, 20% bonds) => ISIN: IE00BMVB5R75

Gold:

- iShares Physical Gold ETC (Gold ETF) => ISIN: IE00B4ND3602

Regardless of your selection, keep in mind the importance of portfolio diversification. Diversification depends on the relationship between assets. For example, if you invest in stocks of 5 banks, are you diversified? Probably not, as they’re companies in the same sector and subject to the same risks.

Where and How to Buy These ETFs?

We’ve already written an article dedicated to the best brokers in Europe. Some options include XTB, DEGIRO, and Trade Republic. We recommend exploring them!

To answer the question of “how to buy these ETFs,” let’s walk through an example using XTB to simulate the purchase of the iShares Core S&P 500 UCITS ETF USD (Acc). After opening an account, here are the steps to buy it:

1st step: search for the ETF

You can do this by name, ISIN, or ticker. Using the ISIN “IE00B5BMR087,” you’ll see two options: one with the ticker CSPX and the other with SXR8. Select “SXR8” as it’s quoted in euros.

2nd step: Click “BUY” (Purchase)

After selecting SXR8, a window will appear at the bottom with a visible “BUY” button. In the middle, you’ll see a “1,” which corresponds to the number of units you want to buy. However, you don’t need to buy a whole unit. You can buy, for example, 0.30 units (fractional shares).

Final step: Complete the transaction

Finally, a window will appear in the middle of the screen to review all values, such as transaction costs (which, in this case, are zero). Then, just click “Confirm”:

Conclusion

With the benefit of automatic income reinvestment and superior tax efficiency, accumulating ETFs are ideal for those looking to maximize capital growth in a simple way.

Throughout this article, we’ve explored the main criteria for choosing the best accumulating ETFs, including low costs, diversification, assets under management, and tax efficiency. We’ve also highlighted practical examples of ETFs suitable for different asset classes and financial goals, as well as simple steps to start investing on accessible platforms.

The “secret” with accumulating ETFs lies in maintaining a disciplined, long-term approach. Remember: investing doesn’t have to be complicated. With the right information and accessible tools, anyone can start building their financial future.

.png)