A Beginner's Guide to Personal Finance in Europe

“The best financial decisions are born from knowledge.”

EU Personal Finance

Financial literacy is one of the most important subjects and one that can have the greatest impact on your life. Unfortunately, it is something rarely taught in schools.

This guide is designed to help you take the first steps toward more conscious financial management in a practical way, adapted to the European reality.

Read, apply, and start transforming your finances today.

1. Where to start?

Creating a budget

The first step to improving your finances is to have a clear and realistic view of how your money is used each month. A well-structured budget helps you identify how much you earn, where you spend, and where you can adjust your expenses. This way, you can free up capital for specific goals, such as building an emergency fund or starting an investment.

How to do it:

- Make a list of all your income sources: Include everything you receive monthly, such as net salary (after taxes and Social Security), extra work income, pensions, or any other source.

- Record all expenses: Divide expenses into categories for a more organized view:

- Fixed: Housing (rent or mortgage), essential utilities (water, electricity, gas, internet), insurance.

- Variable: Food, transportation, healthcare, clothing, leisure, impulse purchases.

- Use financial management tools and apps: You can start with spreadsheets like Excel or Google Sheets, but if you prefer something more automated, there are several apps available in Europe that make daily financial control easier:

- YNAB (You Need A Budget): Helps you assign a purpose to every euro and create a sustainable budget.

- Monefy: Simple and intuitive for tracking daily expenses.

- Toshl: Offers appealing graphs and reminders for your payments.

- Money Lover: Allows you to set savings goals and track your progress.

- Spending Tracker: Minimalist and straightforward, helping you log expenses in just a few seconds.

Practical example (Ana's budget, net monthly salary: €1,600):

After covering all monthly expenses, Ana has €300 available. This margin is a good starting point to build savings, whether for an emergency fund or other financial goals.

Importance of an Emergency Fund

An emergency fund is a financial reserve used to cover unexpected expenses (such as illness, unemployment, or urgent repairs).

Typically, an emergency fund consists of money placed in low-risk, guaranteed-capital investments that can be easily accessed, such as interest-bearing savings accounts, checking accounts, etc.

Besides providing financial security, an emergency fund prevents the need to take out expensive loans or sell long-term investments prematurely.

How much time should my emergency fund cover?

There is no universal formula. In the U.S., it is generally recommended to have at least six months’ worth of expenses - but this figure should not be followed blindly. This concept comes from America, where the financial reality is different from Europe.

In most European countries, due to unemployment benefits and accessible public healthcare (both of which do not exist in the U.S.), some people prefer to keep a smaller reserve, so they do not tie up too much money in low-yield savings products.

Ultimately, you should choose an amount that makes you feel comfortable. A common approach is to keep 3 to 6 months' worth of expenses in a safe and accessible product and invest the rest for the long term. If a major emergency occurs, you can always choose to sell part of your long-term investments to cover an unexpected expense.

The most important thing is to define an amount that gives you peace of mind, without being so high that it prevents you from achieving your other financial goals.

Identifying essential expenses

In an emergency scenario, you won’t maintain the same level of expenses. You can cut back on leisure, non-essential clothing, and impulse purchases. So, from Ana's €1,300 monthly budget, we will distinguish the truly essential expenses.

Example of essential expenses (Ana, in an Emergency Situation):

- Housing: €500

- Essential Utilities (water, electricity, internet, etc.): €120

- Food: €300

- Transportation: €100

- Healthcare: €70

- Minimum Clothing: €20

(Let’s assume that in these circumstances, Ana reduces clothing expenses from €50 to €20, cuts leisure from €100 to €0, and eliminates impulse purchases from €60 to €0.)

Total essential expenses calculation:

€500 (Housing) + €120 (Utilities) + €300 (Food) + €100 (Transportation) + €70 (Healthcare) + €20 (Minimum Clothing) = €1,110 per month.

If the goal is to have an emergency fund for 6 months:

€1,110 x 6 = €6,660

With a monthly savings of €360 (after adjusting the budget), Ana would need approximately 18.5 months to reach the €6,660 goal:

€6,660 / €360 ≈ 18.5 months

Example Table (Ana’s Scenario):

Where should I keep my Emergency Fund?

The emergency fund should be placed in a safe location with high liquidity and low risk. In Europe, you have several options, such as:

- Money market funds: These invest in short-term debt instruments. They have very low volatility, although there is no government guarantee. They can be useful if you want some diversification and potentially greater liquidity.

- Brokerage accounts with interest on uninvested cash: Some brokerages offer interest on idle cash in your account. This option can be convenient if you already use a brokerage, but you should ensure that the institution is solid and understand the terms and conditions.

2. Reducing debt

After establishing a solid budget and starting to build your emergency fund, a crucial next step toward financial stability is addressing the issue of debt. High-interest debts, such as credit cards or personal loans, can consume a significant portion of your income and make it harder to achieve your financial goals. Reducing or eliminating these debts is, in practice, an investment with a guaranteed return: every euro you stop paying in interest is a euro saved.

When can debt be useful?

Not all debt is necessarily negative. A mortgage, for example, can make sense—not only because most people cannot afford to pay for a property upfront, but also because you are acquiring an asset with potential long-term appreciation.

Common types of debt

It is important to understand what type of debt you are dealing with so that you can define an appropriate strategy:

- Personal loans: Unsecured loans, often used to finance one-time expenses. These usually come with higher interest rates.

- Credit cards: A revolving credit option that is convenient in the short term but typically carries very high APRs.

- Mortgage loans: Usually the debt with the lowest interest rate, but it involves a large amount and a long repayment period.

- Auto loans: A loan associated with purchasing a vehicle, sometimes with property reservation clauses.

- Additional mortgages: Extra loans secured by real estate, often with specific conditions and, in some cases, attractive rates—but they require careful consideration.

3. Saving money efficiently

To save more efficiently, you should start by setting concrete goals, analyzing your expenses, finding ways to cut costs, and, most importantly, understanding the power of compound interest.

Setting savings goals

Before you start saving, clarify the why behind it. Define specific goals, categorized by time horizons:

By assigning values, dates, and reasons, you will gain motivation and focus to achieve each of your goals.

Practical tips for saving

- Review service contracts: Negotiate better terms for telecommunications, insurance, and energy. A single phone call might be enough to lower your monthly bill.

- Eliminate unnecessary expenses: Review your active subscriptions and cancel those you don’t use. Also, consider opting for store-brand products, which often offer similar quality at a lower price.

The power of compound interest

Compound interest is "interest on interest." By reinvesting your earnings, your capital grows exponentially over time.

See the power of compound interest—run your own simulations with our compound interest calculator.

Important considerations

- Inflation: With a moderate interest rate, inflation has a significant impact, but the continuous growth of compound interest still helps preserve your purchasing power.

- Management costs: Evaluating the fees associated with financial instruments is essential to maximizing your returns.

We can assume that in a scenario without compound interest, asset growth is linear, limited to annual contributions. However, in a scenario with compound interest, the effect of reinvestment over the years causes the amount to grow exponentially. After 30 years, the investment with compound interest is significantly higher than the scenario without it. Try our compound interest calculator and see the difference!

4. Investments for beginners

After structuring your budget, creating an emergency fund, and working on reducing debt, you can start looking at investing as a way to grow your money in the long term. Investing is not just for the "rich" or "finance experts" - today, with more accessible information and tools, anyone can learn how to invest.

Why invest at all?

Inflation reduces purchasing power over time.

On average, inflation has been around 2% per year since 1999. This aligns with the European Central Bank's target inflation rate and results in a continuous loss of purchasing power.

By investing, you protect your capital and increase the chances of achieving returns higher than inflation. In the medium and long term, investing can help you reach important goals, such as financial independence, buying a home, funding your children's education, or even retiring early.

Risk, return, and diversification

All investments involve some level of risk. Riskier products can offer higher returns but also come with a greater chance of losses. The "secret" is finding the right balance for your investor profile and time horizon.

Risk profiles: Each person has a different risk profile depending on their tolerance for losses and investment timeframe. Here are some typical profiles:

- Conservative: Prefers stability and low volatility. Investments include short-term bonds or money market funds.

- Moderate: Seeks a balance between security and potential returns. A mix of bonds and stocks.

- Aggressive: Accepts higher volatility in exchange for potentially higher returns. Greater exposure to stocks, growth sectors, and emerging markets.

Diversification: Diversifying your capital across different asset classes (stocks, bonds, real estate, etc.), sectors, and regions reduces the impact of a downturn in any single asset, making your portfolio more resilient.

💡 Example: During the 2008 financial crisis, investors who held all their money in stocks lost more than those who had diversified into bonds, global ETFs, and real estate. Diversification helps spread risk.

Time horizon: Time is a Powerful Ally. In the long run, markets tend to appreciate, and short-term volatility becomes less relevant.

- Short-term (<3 years): Term deposits, savings accounts.

- Medium-term (3-10 years): A mix of bonds and some stocks.

- Long-term (>10 years): Greater exposure to stocks, taking advantage of global economic growth.

Table: Example of strategy by time horizon

Time HorizonTypical InvestmentsRiskShort-termTerm deposits, savings accountsLowMedium-termBonds, mixed ETFs (bonds/stocks)ModerateLong-termStocks, diversified global ETFs, BondsModerate/High

Practical example (Impact of long-term investing):

Investing €100 per month in a global ETF for 20 years can result in a significantly higher amount than the €24,000 you would have simply saved without interest. Assuming an average return of 6-8% per year (indicative example), this could grow to around €40,000 or more. While there are no guarantees, historically, global markets tend to grow over the long term.

Where can I invest?

There are numerous investment products, each with different characteristics, risks, and potential returns. Here are some of the most common:

- Stocks: Ownership in companies. They can generate high returns but come with higher volatility. They require research and a willingness to endure market fluctuations.

- Bonds: Loans to governments or companies. Less risky than stocks, they provide more stable but generally lower returns. Ideal for balancing the risk in your portfolio.

- ETFs (Exchange Traded Funds): These are funds traded on stock exchanges that track an index or investment strategy, offering an easy way to diversify your portfolio. ETFs allow exposure to a wide range of assets, such as stocks, bonds, commodities, or specific economic sectors. With low costs and simplified management, ETFs are an ideal solution for beginner investors. For example, you can invest in an ETF that covers global stocks, European bonds, or even commodities, depending on your goals and risk profile.

- Term Deposits: A capital-guaranteed option (up to €100,000 protected by the Deposit Guarantee Fund) with low returns and no volatility. Useful for short- or medium-term goals or the conservative portion of your portfolio.

- Real Estate: Investing in properties (either buying to rent or through real estate funds) can provide regular rental income and potential appreciation. However, it usually requires a larger initial investment and involves maintenance and management costs.

Comparison between investment instruments:

Historical profitability of different financial assets

It is essential to consider the historical returns of each asset class, but don’t forget: past results do not guarantee future performance. Even so, they can provide you with a valuable perspective on what to expect in terms of potential gains and associated risks.

You can run simulations of the historical profitability of different financial instruments using backtesting tools such as Curvo and Portfolio Analyser (developed by us). Please note that the data presented here may not be 100% accurate - if you have any feedback, feel free to reach out to us.

Stocks and bonds

According to a study published in the Credit Suisse Global Investment Returns Yearbook, when analyzing the real returns (adjusted for inflation) of various assets over 122 years, the following average annual values were observed:

- Stocks: 5.3%

- Bonds: 2%

However, keep in mind that there is a relationship between risk and return. In other words, stocks carry a higher risk (volatility) compared to bonds.

Gold

From 1978 to January 2025, gold recorded an approximate average annual return of 6.13%. However, this figure was:

- Just over half of the annual return of global stocks during the same period, and

- Insufficient to cover the average inflation rate in many European countries.

In other words, if you had chosen to keep an investment in gold over that period, you could have seen your purchasing power decline.

ETFs (Exchange-Traded Funds)

ETFs are exchange-traded funds that replicate the performance of an index, sector, or region. For example, if you want to track the performance of the U.S. market, you can invest in an ETF that follows the S&P 500, the main U.S. index composed of 500 of the largest publicly traded companies.

S&P 500

Historically, this index has shown solid growth. From 1988 to the end of 2024, the S&P 500 appreciated by an average of 11.53% per year (in euros, including dividends), far exceeding the average annual inflation rate in Europe.

The table below shows the annualized return of the S&P 500 in euros for various periods:

Source: finance.yahoo.com; investing.com; ecb.europa.eu; koyfin.com

FTSE 100 (United Kingdom)

In Europe, if we look at the FTSE 100, the United Kingdom's main stock index, it has delivered an average annual return of approximately 3.14% since 2000, slightly above the Euro Area's average inflation rate of around 2.44% over the same period.

Cryptocurrencies

In recent years, cryptocurrencies, such as Bitcoin, have gained prominence due to their rapid appreciation. Many investors allocate a substantial portion of their savings to these assets, attracted by the potential for extremely high returns in short periods.

However, it is essential to consider that:

- It is a relatively new market with limited historical data for analysis.

- It exhibits very high volatility, which means a high level of risk.

- Regulation is still limited, increasing uncertainty.

Therefore, if you are considering investing in cryptocurrencies, conduct a careful analysis and always consider diversification, avoiding concentrating a significant portion of your savings in this type of asset.

Costs in different investments

The costs vary depending on the institution and the product, but here are some typical values found in the European and UK markets:

Stocks/ETFs (Online Brokers)

- Brokerage Fees:

- For example, DEGIRO charges around €2 per transaction in certain markets.

- XTB offers 0% commission on European stocks/ETFs up to a certain limit.

- Interactive Brokers charges approximately €1.25 per share in major markets.

- Spread: A small hidden cost between the buying and selling price.

Investment Funds / Pension Plans

- Management Fee: Typically between 0.5% and 2% per year. For example, an actively managed national fund may charge 1.5% to 2% per year.

- Subscription/Redemption Fee: Index funds or pension plans may charge up to 1% upon entry or exit.

ETFs

- TER (Total Expense Ratio): Normally between 0.05% and 0.3% per year for low-cost global ETFs.

- For example, IWDA or VWCE have a TER of around 0.20% per year, much lower than most actively managed funds.

Fixed-Term Deposits

- Generally, no direct costs—just the amount you deposit. However, interest rates are low.

Real Estate

- Taxes (Stamp Duty, Property Transfer Tax - IMT in some countries):

- For example, when buying a €200,000 house, you may pay several thousand euros in taxes (e.g., around €1,800 or more, depending on exemptions and tax brackets).

- Maintenance costs, condominium fees, repairs.

- Real estate agency fees: Typically 5% + VAT on the property price if selling.

Table: Examples of Costs (Approximate values)

(Approximate values and subject to change depending on the institution.)

Whenever you invest, make sure to check the broker’s pricing structure, fund fees, and other costs that may impact your long-term returns.

How to start investing with little money?

Getting started does not require a large fortune. You can begin with small amounts and gradually increase your investments as you gain confidence and knowledge:

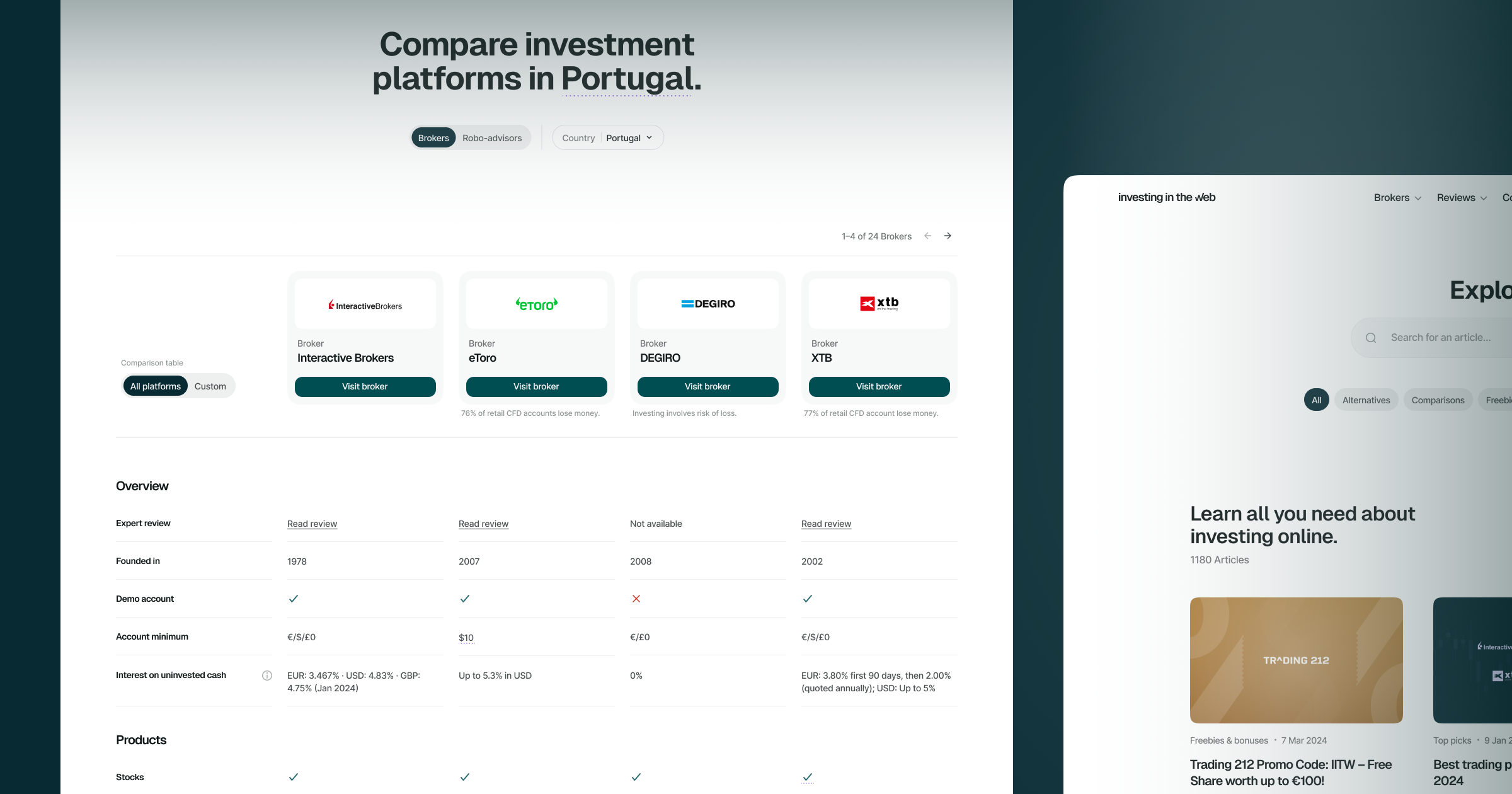

- Online Brokers: Trading 212, Trade Republic, Interactive Brokers, eToro, DEGIRO, XTB, Banco Best, ActivoBank – many offer low or even zero commissions under certain conditions.

- Accessible Investment Funds: Some funds accept investments starting from €100.

- Robo-Advisors: inbestMe, Indexa Capital, Birdee, Openbank Wealth, and other services that build diversified portfolios based on your risk profile.

Practical Example (Step-by-Step Guide to FIRE with an ETF)

- Define Your Goal: You want to achieve financial independence and possibly retire early (FIRE - "Financial Independence, Retire Early"), for example, by the age of 50.

- Decide on a Monthly Investment Amount: Start with €100 per month.

- Open an Account with a Broker: For example, with DEGIRO, XTB, or Interactive Brokers.

- Choose Your Initial Financial Instrument: For a global, long-term investment, you might consider an accumulating ETF (which reinvests dividends), such as:

- VWCE (Vanguard FTSE All-World UCITS ETF): Tracks the FTSE All-World Index, offering exposure to thousands of companies from developed and emerging markets.

- IWDA (iShares Core MSCI World UCITS ETF): Tracks the MSCI World Index, focused on developed countries, covering approximately 1,400 global companies.

- VUAA (Vanguard S&P 500 UCITS ETF): Follows the S&P 500 Index, composed of the 500 largest U.S. companies.

- V60A (Vanguard LifeStrategy 60% Equity UCITS ETF): A balanced portfolio with 60% equities and 40% bonds, investing in funds that replicate global equity and bond indices.

Having multiple options may seem overwhelming, but you can start with just one to simplify the process (e.g., IWDA or VWCE), ensuring global diversification. If you prefer more exposure to the U.S., VUAA is a good choice. If you seek a more balanced mix of stocks and bonds, V60A (Vanguard LifeStrategy) is an interesting alternative. The key: keep it simple in the beginning!

5. How to improve financial education

Financial literacy doesn’t happen overnight - it is built day by day, as you gain more knowledge and experience. By dedicating some time to reading, listening, watching, and participating in educational programs, you will become more confident and secure in your financial decisions.

Explore the resources we've gathered on each topic:

- Recommended Books

- Courses and training programs

- Financial literacy podcasts

- Suggested newsletters

- Online forums and communities

- Recommended YouTube channels

- Financial literacy events

Stay updated – The world never stops

The economy and financial markets are constantly changing. To seize the best opportunities and avoid unpleasant surprises, it’s crucial to stay informed.

Read financial news: Follow sources like Financial Times, the Economist, and others to understand the economic context affecting your savings and investment decisions.

Check official sources: Institutions like the European Central Bank (ECB) publish reports, statistics, and alerts to help you avoid fraudulent financial products.

Use simulators and tools: Try loan calculators, compound interest simulators, FIRE (Financial Independence, Retire Early) models, deposit calculators, pension estimators, and investment tools from banks, brokers, or independent platforms to better understand the impact of your financial choices.

Follow experts on Social Media: Economists, financial advisors, and investors share insights and tips, helping you stay updated effortlessly.

6. The 10 commandments of personal finance

- The best financial decisions are born from knowledge. Knowledge is power. The more you learn about finance, the better your financial decisions will be.

- Slow and steady wins the race. “Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.” - Albert Einstein.

- There’s no such thing as a free lunch. Be wary of promises of high returns with no risk. If something seems too good to be true, it probably is.

- Gambling is the enemy of financial success. Avoid gambling, betting, or other zero-sum games as a financial strategy. These approaches lack long-term sustainability.

- Avoid unnecessary debt. Use credit responsibly. High-interest debt can jeopardize your financial well-being.

- Don’t put all your eggs in one basket. Diversify your assets to minimize risks. Spreading out your wealth across different investments protects you from unexpected market fluctuations.

- Past returns do not guarantee future results. Even if an investment has performed well in the past, it doesn’t ensure it will continue in the same way. Don’t base your decisions solely on historical data.

- Show me the incentive, and I’ll show you the outcome. People and institutions act according to their incentives. Understanding what those incentives are helps predict financial behaviors and outcomes.

- Saving without investing is watching your money disappear. Stashing money away without investing allows inflation to erode its value. Invest to counter the loss of purchasing power and grow your savings.

- Don’t compare investments by returns alone. It’s important to understand the relationship between risk and return. Investments promising very high returns usually involve higher risk.

7. Conclusion

Managing your finances doesn’t have to be an intimidating challenge.

It doesn’t matter if your salary is low or if you’ve accumulated a lot of debt: it’s always possible to regain control of your finances and start building wealth. Small changes, such as adjusting your budget, cutting unnecessary costs, and saving a set amount each month, can make a significant difference in the long run.

If you found this guide useful, share it with friends and family who want a quick and practical approach to personal finance. And if you have any questions, suggestions, or need more information, we’re fully available to help. Get in touch with us and share your feedback.

.avif)