Robinhood pays 5% interest on euros: is it safe?

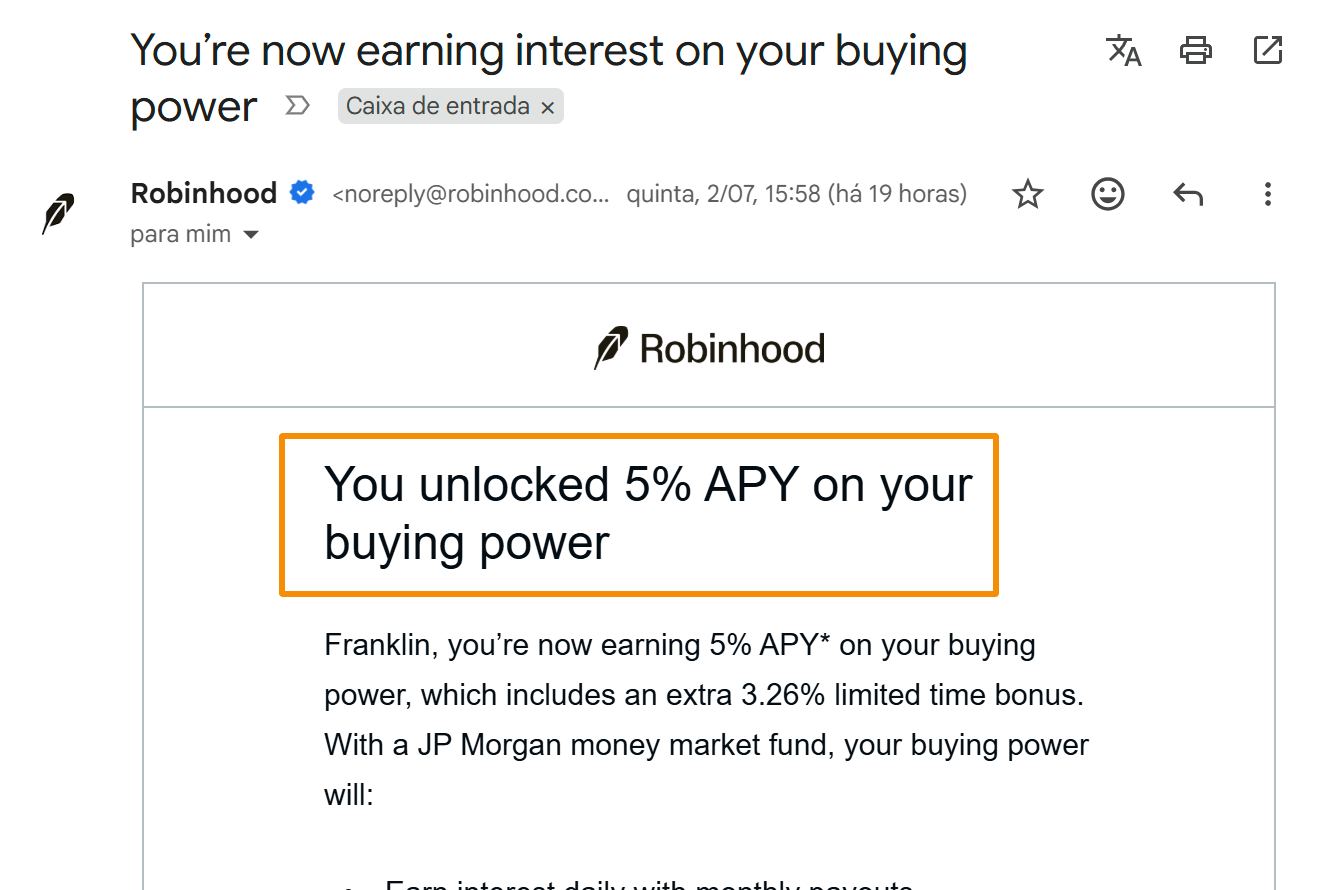

Robinhood has started emailing users about a 5% annual interest rate (APY) on the idle euro cash in their account - and, unlike earlier versions of the offer that ran for a fixed number of months, the latest communication no longer shows a clear end date. Five percent is roughly double what Trade Republic or Trading 212 pay, so the obvious question is: where's the catch? And, more importantly, is your money safe?

The short answer: the offer is legitimate, but it isn't what it looks like at first glance. The 5% is, in large part, a promotional boost that Robinhood can change at any time - the "real and sustainable" rate sits closer to 1.7%. And, crucially, this is not a bank deposit: it's an investment in a fund, with different protection rules from a bank. Let's break it down.

Where does the 5% come from?

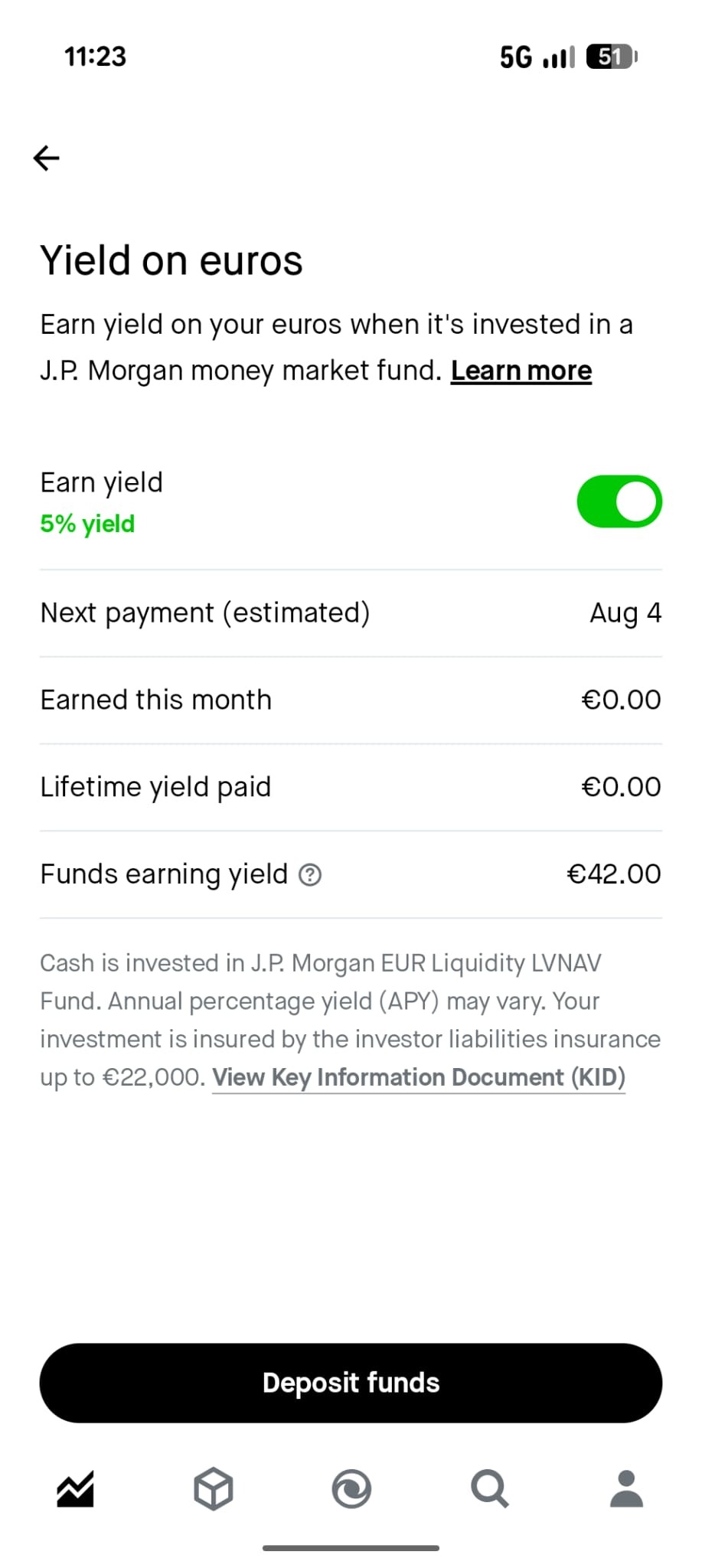

When you turn this feature on, your euro balance is swept once a day into the JPMorgan EUR Liquidity LVNAV Fund (ISIN LU2599140782), a money market fund managed by JP Morgan Asset Management. It's a top-quality fund: AAA-rated by all three major agencies (Fitch, S&P and Moody's), and carrying the lowest possible risk level on the EU regulatory scale (1 out of 7).

According to the fund's own factsheet (May 2026), its 7-day yield was 2.07% and its 30-day average yield was around 2.05%. After the European Central Bank raised its deposit facility rate to 2.25% in June, the fund is likely yielding somewhere around 2.2% to 2.3%. Not 5%.

So how do they get to 5%? Robinhood's own email gives the game away: it calls the extra a "limited time bonus" of 3.26%. Working backwards:

- The "normal" rate, without the bonus: 5% - 3.26% = 1.74%

- And 1.74% is, almost to the cent, the fund's yield (~2.24%) minus Robinhood's 0.50% fee.

In other words: the genuine, durable part of the return is the fund's yield minus the fee. The extra 3.26 percentage points are a subsidy Robinhood pays out of its own pocket to acquire customers.

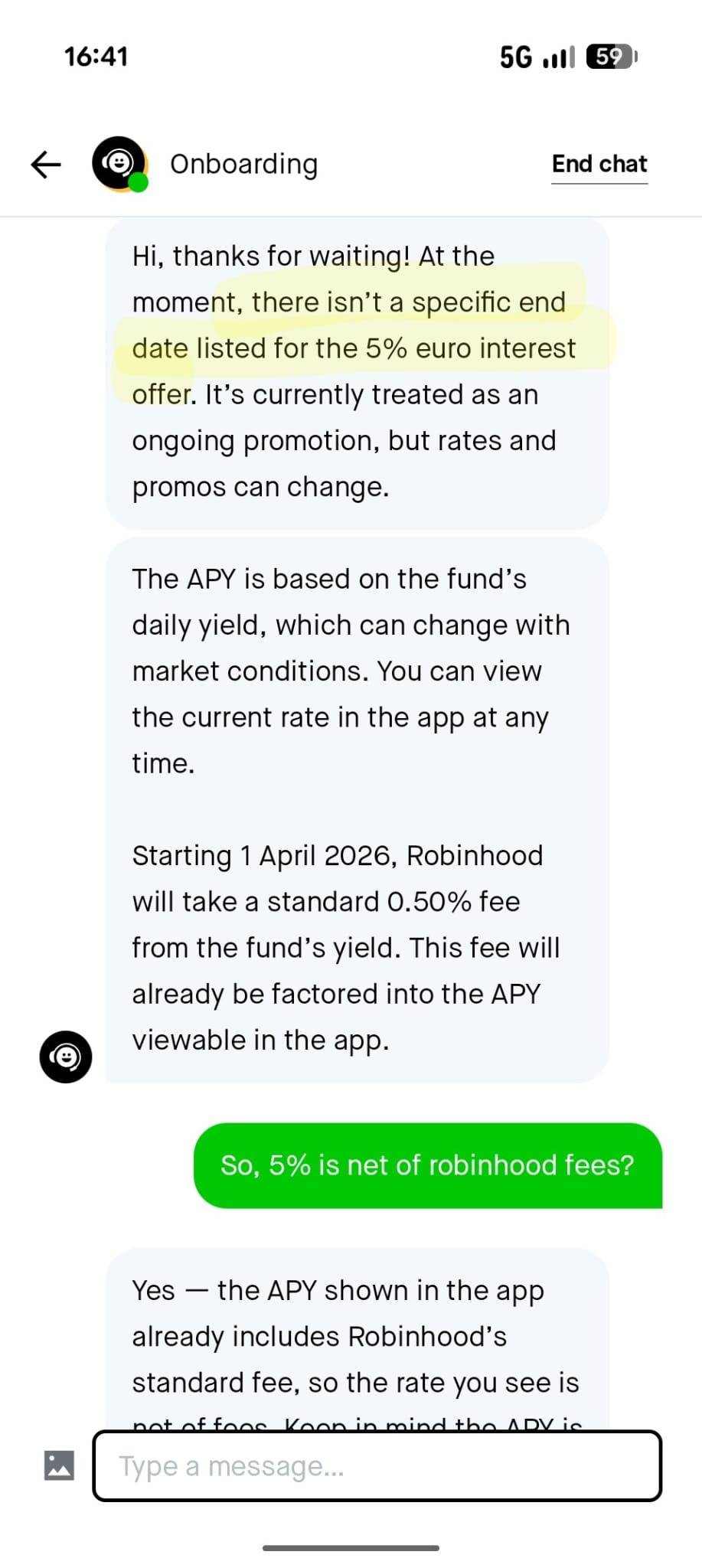

There's a contradiction worth flagging here. When we contacted support, we were told there is no defined end date for the offer:

But the email itself refers to a "limited time bonus" and a promotion that "ends" - and even shows an end date with a formatting bug ("1 Jan., 0001"). In practice, what matters is that this is a variable rate: with or without a set date, Robinhood can cut it whenever it wants. Counting on 5% over the long term is very likely a mistake.

The 5% still has a 0.50% fee along the way

Robinhood charges a 0.50% fee (50 basis points) on the fund's annual yield. It's important to understand what this does: it permanently reduces your return by half a percentage point versus what the fund earns.

During the promotion, Robinhood says the rate shown in-app is already net of this fee (the bonus more than covers it). The catch is what comes "after": once the 3.26-point bonus disappears, you're left with the fund's yield minus the 0.50% - i.e. something in the region of 1.7% at today's rates. Less than most of the alternatives available to European savers.

There's also a technical detail worth knowing: interest accrues daily but does not compound (it's paid monthly on your balance, with no interest on interest). So despite being advertised as "APY", in practice it behaves more like a simple annualised yield.

Is it safe? Regulation and the €22,000 protection

The entity behind the offer is Robinhood Europe, UAB (RHEU), Robinhood's European subsidiary, based in Vilnius, Lithuania (company code 306377915). It is authorised and supervised by the Bank of Lithuania (Lietuvos bankas), the country's financial regulator. It's a real, regulated EU entity - that part isn't in doubt. If you want the full picture of the European product, see our Robinhood Europe review.

What is in question is the nature of the protection. Robinhood's communication says the investment is protected "up to €22,000". This is not the €100,000 deposit guarantee you get at a bank. It's the Lithuanian investor compensation scheme, run by the Deposit and Investment Insurance public institution. And there are two fundamental differences:

- It only covers the firm failing. This scheme only kicks in if Robinhood Europe is unable to return the money or securities that belong to you - for example, through insolvency or administrative failure. The regulator itself is explicit: investment risk (the possibility that the investment loses value) is not covered. If the fund falls in value, the loss is yours.

- It's an investment, not a deposit. Because you're investing in a money market fund rather than depositing money at a bank, the €100,000 deposit guarantee does not apply. At most, this €22,000 cap applies - and only if the firm fails. This is a general rule: money market funds sit under an investor compensation scheme, not a deposit guarantee scheme.

In practice, the market risk of a fund like this is very low (it's literally the most conservative investment product there is, with the top rating). But "very low" isn't "zero". In extreme market conditions, a money market fund can have zero or even negative returns, and there's no capital guarantee. That's the difference between "safe like a deposit" and "safe like a conservative investment".

How does it compare with Trade Republic and Trading 212?

Strip out the bonus and Robinhood's base offer trails its closest competitors. Here's the essential comparison:

The takeaway is clear. Trade Republic, being a bank regulated in Germany (BaFin and the Bundesbank), offers the "strong" €100,000 protection on your cash balance - the same as a current account. Trading 212 pays 2.40% (up to 3.50% for new clients in selected countries) and keeps much of the cash on deposit with J.P. Morgan SE, also with €100,000 coverage on that portion. For the full landscape, see our guide to the best euro savings options across Europe.

Robinhood has the highest headline rate today thanks to the subsidy - but once that ends, it's left with the lowest rate of the three, and the weakest form of protection (€22,000, and only for firm failure).

Don't forget the tax

Robinhood does not withhold tax on the interest it pays. That means the interest is taxable in your country of residence and it's your responsibility to declare it in your annual tax return - Robinhood won't do it for you. Under the Common Reporting Standard (CRS), your national tax authority may already receive data about the account, so declaring it properly matters. The exact rate and reporting rules depend on where you live, and for some investors the extra admin can eat into the headline advantage.

Verdict: is it worth it?

The offer is real, and the money sits in one of the most solid money market funds in the world. But the 5% is, above all, a marketing hook. Three points to remember:

- The 5% rests on a bonus that can vanish. The sustainable rate sits around 1.7% (the fund's yield minus the 0.50% fee), below both Trade Republic and Trading 212.

- This is an investment, not a deposit. Protection is €22,000 under Lithuania's investor compensation scheme, and it covers the firm failing - not market losses. Don't confuse it with the €100,000 deposit guarantee.

- If this is for your emergency fund, the combination of a lower base rate, €22,000 protection and self-reported tax makes the offer less attractive than it appears.

If you already use Robinhood in Europe (for crypto or Stock Tokens), taking advantage of the bonus while it lasts can make sense for small amounts. But moving the bulk of your savings there in the belief that it's "5% guaranteed and safe like a bank" starts from a false premise.

This offer has generated plenty of discussion in the r/eupersonalfinance community, where the consensus echoes the analysis here: the underlying fund is solid and the rate is real, but it's a promotional rate in a neo-broker price war that can be cut at any time - and the €22,000 covers the firm failing, not the fund losing value.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Investing involves risk, including the potential loss of your invested capital.