Saxo review 2026: is it the best European broker for you?

In this article, we review Saxo, a Danish investment bank founded in 1992, to help you decide whether it is the right broker for your investment goals in Europe.

Over the last few years, Saxo has transformed itself from a trading-first platform into one of Europe's most compelling brokers for long-term investors. In 2024 and 2025, the company rolled out a deep pricing overhaul: custody fees were removed across core European markets, inactivity fees disappeared entirely, and trading commissions dropped to levels that are now competitive with, and sometimes lower than, Interactive Brokers (read our full IBKR review). In parallel, Saxo launched the SaxoInvestor interface, which gives passive ETF investors a cleaner experience than IBKR's platform.

Two other developments matter for European investors. First, in 2025 the Swiss private banking group J. Safra Sarasin acquired a controlling stake of approximately 70% in Saxo, replacing the previous Chinese majority owner. Second, S&P Global Ratings reaffirmed Saxo's A- long-term rating with stable outlook in March 2026. For European investors, this combination (Swiss ownership, Danish regulation, A- rating, SIFI status in Denmark) offers genuine counterparty diversification away from US-domiciled platforms. In an era of trade tensions, that is not a minor consideration.

Saxo gives you access to over 71,000 instruments across ~50 global exchanges: stocks, ETFs, mutual funds, bonds, options, futures, CFDs, forex, and commodities. The product breadth and the depth of regulatory backing are difficult to match in the European retail brokerage space.

Disclosure: This article is for informational purposes only and does not constitute financial advice. We have no active commercial partnership with Saxo at the time of writing.

Overview

Saxo was founded in 1992 in Copenhagen by Kim Fournais and Lars Seier Christensen, originally as Midas Fondsmæglerselskab. In 2001, the company obtained a banking licence and rebranded as Saxo Bank. Today, the legal entity is Saxo Bank A/S, but the commercial brand has been simplified to just "Saxo".

Saxo currently serves around 1.5 million clients globally, manages over 115 billion USD in client assets, and handles 15+ billion EUR in daily trade volume. It operates in more than 15 jurisdictions and is regulated by 15+ financial authorities.

Unlike many multi-asset brokers that offer only CFDs across asset classes, Saxo provides direct access to the underlying securities themselves:

- Stocks on ~30 exchanges (including hard-to-access markets like Malaysia)

- ETFs (with automatic savings plans in some countries)

- Mutual funds and managed portfolios

- Government and corporate bonds

- Options and futures on multiple exchanges

- Forex and CFDs

- Commodities

In June 2023, Saxo Bank A/S was designated a Systemically Important Financial Institution (SIFI) in Denmark by the Danish FSA. This is not a guarantee of state intervention in case of difficulties, but it implies higher capital requirements, enhanced regulatory oversight, and a higher probability of state involvement should it ever be needed.

Highlights

Pros and cons

Pros

- Bank-licensed in three European jurisdictions (Denmark, Netherlands, Switzerland)

- A- credit rating from S&P (stable outlook) and SIFI status in Denmark

- Swiss majority ownership via J. Safra Sarasin Group (since 2025)

- Huge product breadth (71,000+ instruments, ~50 exchanges)

- Two purpose-built platforms (SaxoInvestor for passive investors; SaxoTrader for active traders)

- Competitive trading commissions after the 2024-2025 pricing overhaul

- Stock lending program available across most markets with 50/50 revenue split

- No inactivity fees

- Custody fees removed in most core European markets

- Long track record (founded in 1992)

Cons

- Pricing structure is complex - varies significantly by country, exchange, and account tier

- FX conversion fee (0.25%) is well above Interactive Brokers (~0.002%)

- Custody fees still apply in non-core markets (e.g., Portugal, Norway, UK on ETFs)

- Interest on cash is 0% for Classic and Platinum tiers - only VIP (€1M+ deposit) earns meaningful rates

- High minimum deposit in some countries (e.g., €100,000 in Spain and Portugal)

- PRIIPs restrictions on US-listed ETFs (no workaround unless you qualify as elective professional)

- Does not accept US residents

- SaxoTrader can feel intimidating for absolute beginners

Where Saxo is most competitive: the core markets

Saxo's 2024-2025 pricing overhaul was not applied uniformly across all countries. The company defined a list of core markets, countries where it competes hardest for retail clients, and removed custody fees there entirely. In non-core markets, custody fees of 0.09% to 0.15% per year may still apply.

This means your experience as a Saxo client depends materially on where you live. Here is the current map:

If you live in one of the green core markets (Belgium, France, Italy, Netherlands, Poland, Switzerland, Denmark, or with a sec. lending opt-in in Czech Republic), the Saxo direct experience is substantially better than in non-core markets. For investors in Spain, Portugal, or the UK, the cost gap with Interactive Brokers widens significantly due to ongoing custody fees.

Trading platforms

Important clarification: Saxo used to offer three platforms - SaxoTraderGO, SaxoTraderPRO, and SaxoInvestor. In 2025-2026, the company unified the brand into two platforms:

- SaxoInvestor - simple, focused on long-term investors

- SaxoTrader - advanced, available on web, mobile, and desktop (replaces both SaxoTraderGO and SaxoTraderPRO)

With a single Saxo account, you get access to both and can switch freely between them.

SaxoInvestor

The SaxoInvestor platform is built for the passive investor - someone buying ETFs or mutual funds on a monthly or quarterly schedule who does not need advanced charting. Features include:

- Access to stocks, ETFs, mutual funds, and bonds

- Clean, portfolio-focused interface

- Web and mobile versions

- Simple portfolio analysis and performance reports

- No access to derivatives (options, CFDs, futures) - by design

For ETF-focused long-term investors, this is the right interface. The absence of derivatives is actually a feature, not a bug - it removes temptation.

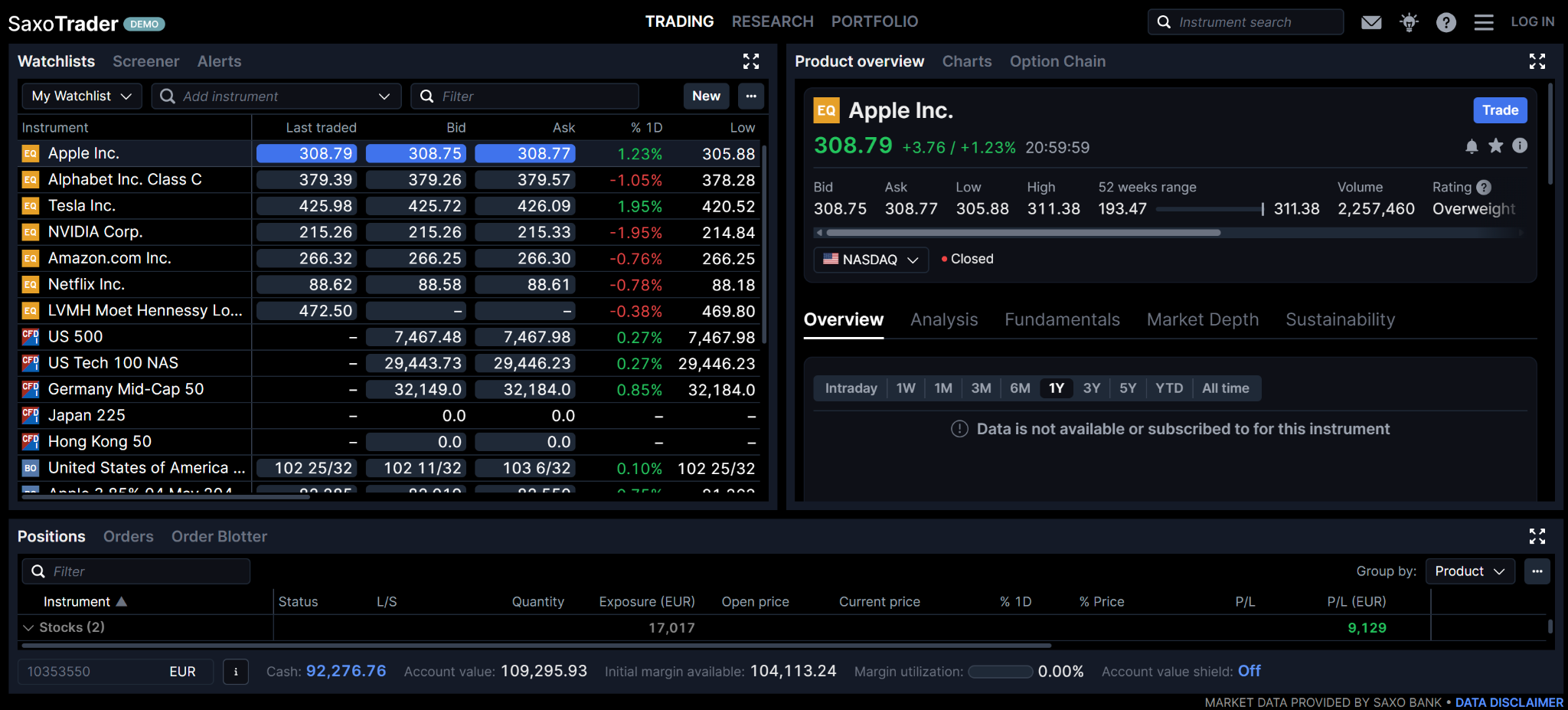

SaxoTrader

The SaxoTrader platform is the advanced platform, available on web, mobile, and desktop. It replaces the older SaxoTraderGO and SaxoTraderPRO branding. Features include:

- Access to the full product range (including options, futures, CFDs, and forex)

- Advanced charting and technical analysis

- Multi-screen layouts on desktop

- Risk management tools

- API access for algorithmic trading and integrations

- Margin trading and Lombard loans (where available)

In our testing, the SaxoTrader desktop platform is one of the best professional-grade platforms in the European market - comparable to Interactive Brokers' TWS, but generally considered more polished in terms of visual design and information hierarchy.

Third-party platforms

Saxo can also be accessed via TradingView, which appeals to chart-focused retail investors. Other third-party integrations (MetaTrader, FIX/API) are oriented towards professional and institutional clients.

Demo accounts

Saxo offers free 20-day demo accounts for both platforms. We recommend testing both before opening a funded account, especially because the right platform choice depends heavily on your investment style.

Products and markets

Saxo's product breadth is one of its strongest differentiators. Depending on your country of residence, you can access over 71,000 instruments, including:

- Stocks across ~30 exchanges worldwide

- ETFs (UCITS for European retail investors)

- ETCs (Exchange-Traded Commodities)

- Listed options on multiple exchanges

- Futures contracts across asset classes

- Government and corporate bonds

- Mutual funds and managed portfolios

- Forex spot and forwards

- CFDs across stocks, indices, commodities, FX, and crypto

US-listed ETFs and PRIIPs

As a European broker, Saxo follows PRIIPs regulations strictly. This means that, as a retail client, you cannot buy most US-listed ETFs (like VOO, VTI, or VTSAX) due to the lack of translated KID documents. The same restriction applies to all PRIIPs-compliant brokers in Europe (see also our guide to UCITS ETFs vs US ETFs).

There are two workarounds. First, in smaller CEE markets (Bulgaria, Croatia, Greece, Hungary, Lithuania, Romania, Slovakia, Slovenia), ETF issuers like Xtrackers offer equivalents to popular Vanguard ETFs. Second, qualifying as an elective professional client unlocks access to US ETFs and higher leverage. The "2 out of 3" test requires:

- A portfolio of financial instruments above €500,000

- An average of 10 significant trades per quarter over the last 12 months

- At least one year of professional experience in the financial sector requiring knowledge of the relevant products

Important: opting for elective professional status means you give up some retail investor protections (lower leverage caps, negative balance protection, ICSD compensation thresholds in some cases). Understand the trade-off before applying.

Tax wrappers

In several European markets, Saxo supports local tax-advantaged accounts:

Earn extra income with stock lending

Saxo offers a stock lending program that lets you generate additional passive income by lending out the stocks and ETFs in your portfolio. This feature is increasingly common among premium brokers, and Saxo's implementation is well thought out for retail investors.

How it works

When you activate stock lending, Saxo lends out your eligible securities to other market participants, typically hedge funds or institutional traders who want to short the stock, hedge existing positions, or meet delivery deadlines. In return, the borrower pays interest, and Saxo splits the revenue with you on a 50/50 basis.

Example: if you own shares of a stock currently in high demand with a 24% annual borrow rate, Saxo lends them out and you receive 12% per year (50% of the 24%) while your shares are lent. The income is credited to your account at the end of each month, and you can track everything in the stock lending dashboard.

Recent examples

As an illustration, here are the annualised interest rates Saxo clients earned on selected high-demand stocks in January 2026:

Important caveats: the lending rate varies stock by stock based on market demand, and the actual lending of your shares is not guaranteed, it depends on whether anyone is willing to borrow them. Past returns are not a reliable indicator of future income. For the majority of broad-market ETFs and large-cap stocks, lending rates tend to be very low (often below 0.5% annualised).

Key features

- Activate or deactivate the service at any time from your Portfolio overview

- Your shares remain in your portfolio and you can sell them at any moment

- You receive payments equivalent to applicable dividends while shares are lent

- Saxo posts collateral of at least 102% of the value of the open loan to protect you

- Earnings appear in your account at the end of each month

- All eligible stocks/ETFs in your account become available when you activate the service (you cannot cherry-pick)

Risks to understand

Stock lending is not free of risk. There are three key considerations:

- Voting rights: while your shares are lent out, you forfeit voting rights and the ability to attend shareholder meetings

- Market risk: you still bear the full market risk of the securities lent (your account value still moves with the share price)

- Counterparty risk: in the unlikely event of Saxo's bankruptcy, there is a period between insolvency and collateral distribution where the value of the open loan could exceed the collateral. The 102% minimum collateral reduces but does not eliminate this risk

Saxo publishes the full terms in the Securities Lending Agreement. For most long-term passive investors, the upside of activating stock lending generally outweighs the risks - particularly because the income is uncorrelated with market returns. But you should read the terms before opting in.

How it compares to competitors

Saxo's 50/50 revenue split is identical to Interactive Brokers' Stock Yield Enhancement Program (SYEP). The key difference is that Saxo has no minimum account size for activation, whereas IBKR's program requires at least $50,000 in equity. For smaller portfolios, this makes Saxo's stock lending more accessible than IBKR's.

Fees and commissions

Saxo operates a three-tier account system based on the amount deposited:

- Classic - minimum deposit varies by country (€0 in most core markets)

- Platinum - minimum deposit of $200,000 - lower commissions

- VIP - minimum deposit of $1,000,000 - lowest commissions and dedicated relationship manager

The higher your tier, the lower your trading fees. For most retail investors, Classic is the starting point.

Stock and ETF commissions

These commissions are competitive across all major European exchanges. For Euronext, the most relevant exchange for many European long-term ETF investors, Saxo's €2 minimum fee is lower than Interactive Brokers' fixed plan minimum of €3, though IBKR's tiered plan can still be slightly cheaper for very small orders.

FX conversion fees

Saxo charges 0.25% on currency conversions in most countries. In the UK, the FX fee is tiered by account level: 0.6% (Classic) / 0.4% (Platinum) / 0.2% (VIP).

This is significantly higher than Interactive Brokers' ~0.002% (with a $2 minimum), but in line with most other European brokers. If you frequently trade in non-EUR currencies, consider holding cash balances in those currencies on the platform to avoid repeated conversions.

Custody fees

As covered in the core markets section above, custody fees were removed from most core European markets in 2024-2025. In non-core markets, custody ranges from 0.05% to 0.15% per year depending on account tier.

Quick rule of thumb: if you live in Belgium, France, Italy, the Netherlands, Switzerland, Denmark, or Poland, you typically do not pay custody fees. If you live in Portugal, Spain, the UK (for ETFs), or Norway, you do.

Other fees

- Inactivity: €/$/£0 (removed in 2024)

- Deposits: €/$/£0

- Withdrawals: €/$/£0

- CFD financing: spread + overnight interest

- Forex spread: variable by pair and account tier

Interest on uninvested cash

Saxo pays interest on uninvested cash, but the rates depend heavily on your account tier. As of 21 May 2026, on a balance of 150,000 in the relevant currency:

Interest rate tables - EUR, USD, GBP across Classic/Platinum/VIP tiers

The practical takeaway: for Classic and Platinum clients, interest on uninvested cash is zero. Only VIP clients (€1M+ deposit) receive meaningful interest. If earning interest on your cash balance is important to you, Interactive Brokers remains a better option, IBKR pays interest from much smaller balances (€10,000+) at competitive rates across all account types.

Total cost simulation: Saxo vs Interactive Brokers vs Swissquote

To make the cost comparison concrete, consider a typical long-term passive investor: €100,000 initial investment + €1,000/month into a UCITS ETF on Euronext over 10 years. Assuming no custody fees (core market scenario):

In core markets, Saxo edges out IBKR thanks to the lower €2 minimum on Euronext (vs IBKR's €3 fixed-plan minimum, or the percentage-based tiered fee). Over 10 years, the difference between Saxo and IBKR is around €89, meaningful but not transformative. The gap to Swissquote, on the other hand, is nearly €1,600.

Important caveat: if you live in a non-core market (UK ETFs, Portugal, Spain, Norway), Saxo's 0.09%-0.15% annual custody fee would add roughly €1,500-€2,500 to the 10-year cost on a €100,000 portfolio, making IBKR substantially cheaper in those markets.

Regulation and safety

Saxo's regulatory profile is one of the strongest among European retail brokers. Three points stand out.

Three European banking licences

Saxo operates as a fully licensed bank in three European jurisdictions:

- Denmark - Saxo Bank A/S, regulated by the Danish FSA (primary entity for most EU clients)

- Netherlands - Saxo Bank NL, regulated by De Nederlandsche Bank (DNB) and AFM (handles Belgian, French, and Dutch clients)

- Switzerland - Saxo Bank Switzerland, regulated by FINMA

Other jurisdictions where Saxo holds local regulatory licences include the UK (FCA), Italy (CONSOB), Singapore (MAS), Australia (ASIC), Hong Kong (SFC), Japan (JFSA), and the UAE (DFSA). The full list is available on the Saxo Licences and regulation page.

SIFI status and A- credit rating

In June 2023, the Danish FSA designated Saxo Bank A/S as a Systemically Important Financial Institution (SIFI) in Denmark. This carries three practical implications:

- Higher minimum capital requirements (Total Capital Ratio of 24.8% as of 2025)

- Enhanced regulatory supervision

- Higher probability of state intervention in case of distress (though not a guarantee)

In addition, S&P Global Ratings reaffirmed Saxo's A- long-term rating with stable outlook in March 2026. Historically, A- rated financial institutions have an estimated 10-year probability of default of around 1-2% - a very low risk level. For comparison, Interactive Brokers Ireland Limited holds the same A- rating.

Investor protection

The investor protection scheme depends on the Saxo entity holding your account:

Beyond these schemes, all client assets are segregated from Saxo's own assets, as required by EU regulation. Even in a Saxo insolvency, your securities are not part of the bankruptcy estate.

Ownership structure

In 2025, the Swiss private banking group J. Safra Sarasin acquired approximately 70% of Saxo Bank A/S, replacing the previous Chinese majority owner (Geely). The deal closed in 2025, with founder and CEO Kim Fournais retaining a significant minority stake and continuing to lead the company.

From a European investor's perspective, this matters for three reasons:

- Geographic risk diversification - Swiss ownership reduces exposure to US-China geopolitical tensions

- Stronger European identity - aligns Saxo with the Swiss tradition of conservative private banking

- Operational continuity - Fournais remains at the helm, minimising disruption to strategy and culture

Financial transparency

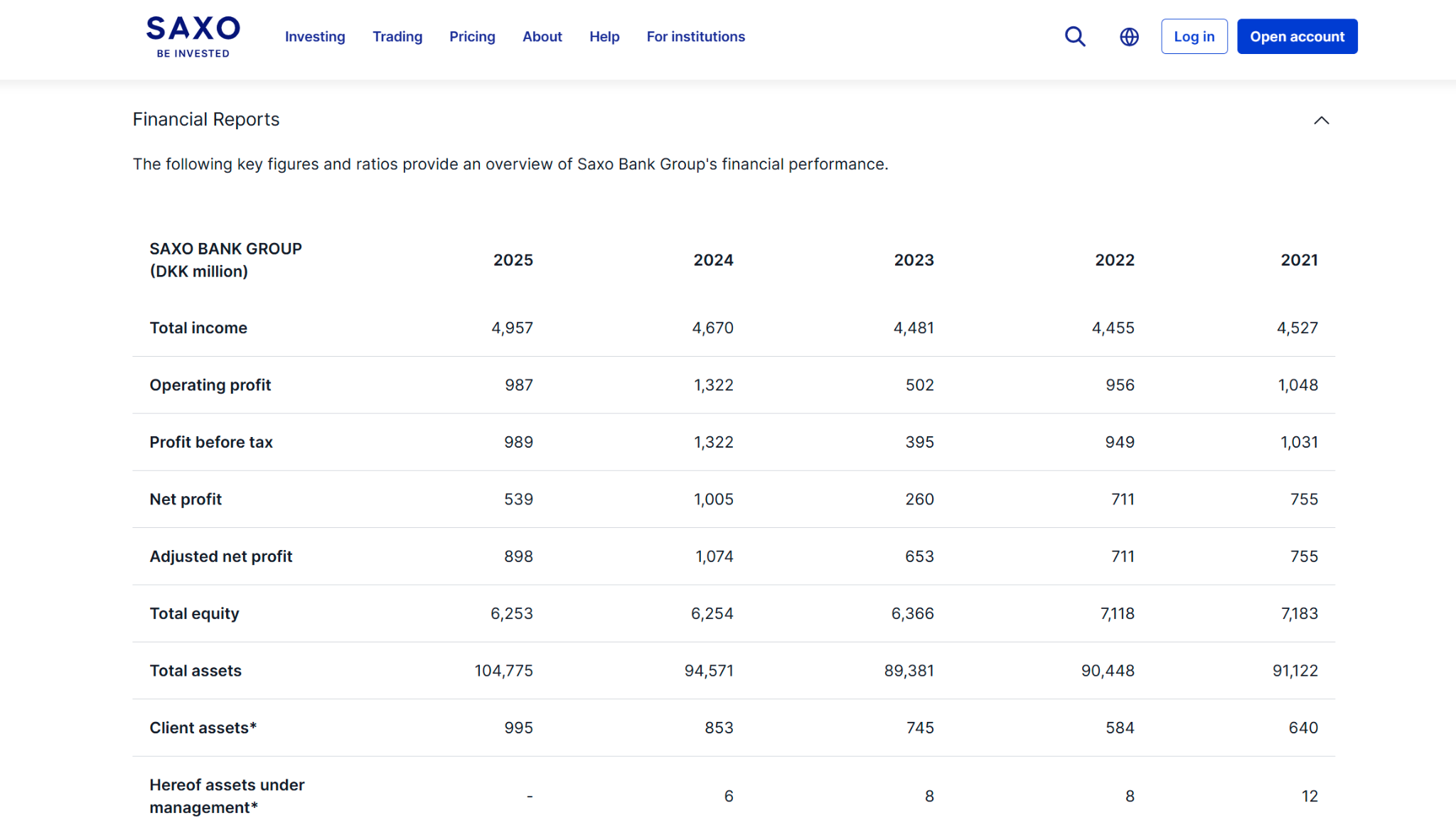

Although a private company, Saxo publishes detailed financial reports on its Investor Relations page. Here is a snapshot of the Saxo Bank Group 2025 results:

The 2025 numbers show continued top-line growth (revenue +6.1% YoY) alongside a compression in net profit, reflecting both transition costs from the ownership change and ongoing investment in platform infrastructure. The total capital ratio of 24.8% remains well above regulatory minimums.

Account opening

Opening an account with Saxo is straightforward and entirely online. The process typically takes around 15 minutes for the application, followed by a verification period of 1-3 business days.

Step-by-step

- Go to home.saxo and click "Open account"

- Select your country of residence

- Complete the personal data section (name, address, tax ID, employment)

- Complete the MiFID II knowledge and experience questionnaire

- Upload verification documents (passport or ID + proof of address)

- Wait for account approval (1-3 business days)

- Fund your account via wire transfer (no credit/debit cards in most markets)

- Access SaxoInvestor and SaxoTrader with the same login

Minimum deposit by country (illustrative): €0 in most core markets (Belgium, France, Italy, Netherlands, Poland, Switzerland, Denmark, Singapore, UK); €5,000 in MENA countries (UAE, Qatar, Saudi Arabia); €100,000 in Spain and Portugal.

Customer support

Customer support quality at Saxo is generally well-regarded, particularly compared to lower-cost competitors. Support is available via:

- Phone (during European business hours)

- Live chat (during business hours)

- Help centre with detailed articles

Languages: English is the default for international clients. Local-language support is available in core markets (French, Italian, Dutch, Danish, Polish, German, etc.). Note: Portuguese is only available for VIP clients (€1M+ deposit).

In our experience, response times via phone are usually under 5 minutes, and email queries are typically resolved within one business day. This is markedly better than the support experience reported by IBKR users, particularly for non-technical questions.

Who is Saxo for?

Saxo makes the most sense for three investor profiles in Europe:

Profile 1: long-term ETF investor in a core market

If you live in Belgium, France, Italy, the Netherlands, Switzerland, Denmark, or Poland, the Saxo direct experience is excellent. You get a clean SaxoInvestor interface, competitive Euronext or Xetra commissions, no custody fees, and access to local tax wrappers (PEA, Aktiesparekonto, regime amministrato, etc.). For passive ETF investors in these countries, Saxo is often the best all-rounder available.

Profile 2: investor seeking counterparty diversification

If you already have an account at Interactive Brokers, Trading 212, or DEGIRO, adding Saxo to the mix gives you genuine counterparty diversification. Swiss ownership, Danish regulation, A- rating, and SIFI status form a profile that is structurally different from US-domiciled platforms. In stressed market scenarios, this diversification matters more than it appears in calm times.

Profile 3: semi-active or professional trader

If you trade options, futures, CFDs, or forex alongside long-term holdings, the SaxoTrader desktop platform competes with the best in Europe. The product breadth (71,000+ instruments, ~50 exchanges) and the ability to qualify as elective professional client unlock features that most retail-focused brokers simply do not offer.

Who Saxo is not for

- Investors in non-core markets (Portugal, Spain, UK ETFs, Norway) who prioritise low total cost over institutional solidity - IBKR is generally cheaper after factoring in custody fees

- Investors who frequently convert between currencies (the 0.25% FX fee adds up)

- Investors who want meaningful interest on uninvested cash without depositing €1M (Classic and Platinum earn 0%)

- US residents (not accepted)

- Beginners who feel intimidated by complex pricing structures and three-tier account systems

Alternatives to Saxo

If Saxo doesn't quite fit your needs, three other European brokers are worth comparing. See also our overview of the best trading platforms in Europe for a broader view.

Final verdict: is Saxo worth it in 2026?

Saxo is one of the most institutionally solid retail brokers in Europe. Three European banking licences, A- credit rating with stable outlook, SIFI status in Denmark, and Swiss majority ownership via J. Safra Sarasin form a profile that is genuinely hard to match in the European retail space. The 2024-2025 pricing overhaul has eliminated most of the historical cost disadvantages, the SaxoInvestor and SaxoTrader platforms are excellent, and the stock lending program adds a meaningful income stream for long-term holders.

That said, Saxo is not the right broker for every European investor. The answer depends on three questions:

- Do you live in a Saxo core market? If yes (Belgium, France, Italy, Netherlands, Switzerland, Denmark, Poland), Saxo direct is excellent and often beats IBKR on Euronext minimums. If no (Spain, Portugal, UK on ETFs, Norway), custody fees materially erode Saxo's cost competitiveness vs IBKR

- Do you value institutional solidity above pure cost minimisation? Saxo wins on the safety-and-platform-quality axis. IBKR wins on cost, FX, and interest on uninvested cash

- Do you trade more than just ETFs? If you use options, futures, CFDs, or forex alongside long-term holdings, SaxoTrader is one of the best platforms in Europe and the product breadth justifies the platform choice on its own merits

Our recommendation: for long-term ETF investors in Saxo core markets, Saxo is a strong default choice and often the best all-rounder. For investors in non-core markets focused on cost minimisation, Interactive Brokers remains hard to beat. And for investors building a multi-broker setup for counterparty diversification, Saxo is one of the few European-regulated, bank-licensed options that genuinely complements US-domiciled platforms.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Investing involves risk, including the potential loss of your invested capital. Do your own research and consider seeking advice from a qualified financial professional before making investment decisions.

.png)